Look, we've all been there. You’re running a prominent regional bank that holds an outsized amount of uninsured deposits, which are overly concentrated in the tech sector, all while holding a huge, unhedged, long-dated bond portfolio that has taken a major hit over the past year due to rising interest rates. Then you’re forced to sell that portfolio, realizing a major loss, to provide liquidity to your depositors who need to withdraw their money to pay their bills after venture capital stops flowing. The major loss leads to a modern-day bank run and seizure of the bank by U.S. regulators, creating a domino effect that causes another bank failure and widespread concerns over systemic risk of the banking system. Of course, this may not describe you exactly, but the story may sound familiar, and you may be wondering if the uncertainty in the banking system affects you. The answer is probably a familiar one: maybe.

Banks are tightening their credit standards to hold more liquid assets on their balance sheets, so they may be less willing to lend out . However, credit has been tightening for over a year now as interest rates have risen, and banks also often sell their mortgages by way of Mortgage-Backed Securities (MBS), so they don’t have to hold the long-term loans on their balance sheets. If a creditworthy homebuyer qualified for a loan before the bank failures, they almost surely still qualify today. In the short term, we don’t expect major mortgage rate moves due to the Silicon Valley Bank and Signature Bank failures.

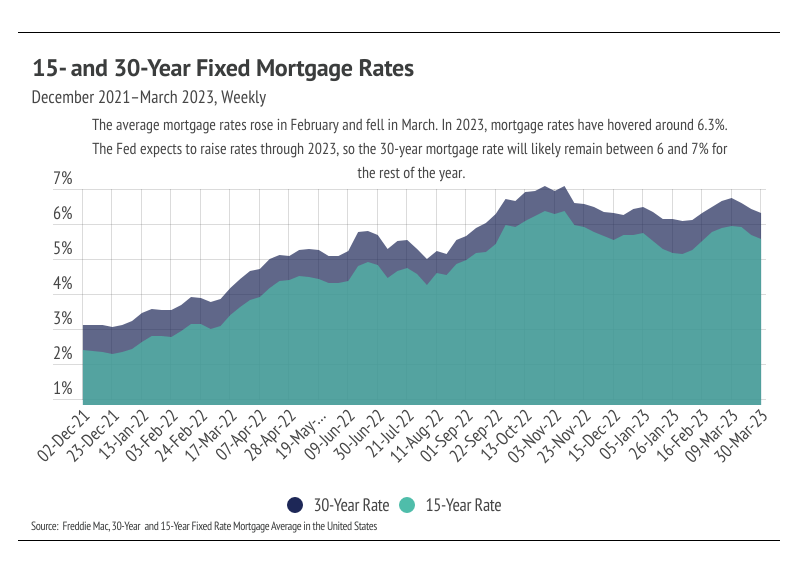

The Fed, which coincidentally met right after the bank failures, chose to raise their benchmark rate by 0.25%, rather than the anticipated 0.50%, in a continuing effort to combat inflation. The Fed chose the smaller 0.25% hike because banks were already tightening after the bank failures, so the Fed had less of a need to do so as well. Inflation is still well above the 2% target, although it’s coming down steadily. At the current rate at which inflation is dropping, it should be back to the target rate in about a year. One caveat that could slow declining inflation is OPEC’s surprise announcement that they are cutting oil production, which will cause gas prices to increase over the next few months. All this to say, interest rates will remain elevated and volatile over the next 12 months, and, more specifically, mortgage rates will likely hover around 6-7%.

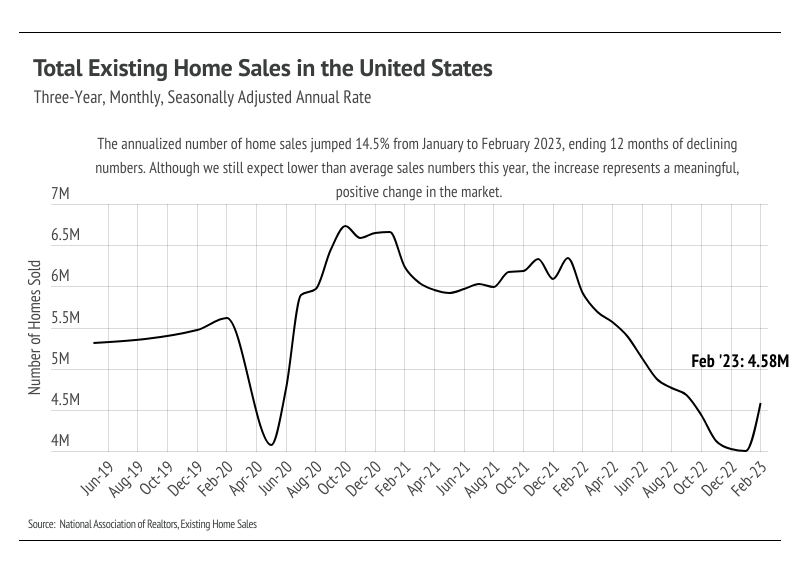

The 30-year average mortgage rate has been above 6% for six months now, and a significant number of buyers are finally coming back to the market. According to the National Association of Realtors (NAR), sales jumped 14.5% in February, the largest month-over-month increase since July 2020, breaking the 12-month streak of declining sales. We attribute three main factors to the increase: (1) the initial sticker shock of higher rates has worn off, (2) the time before buyers refinance has shortened, and (3) typical seasonality has returned. As rates shot up in 2022, affordability plummeted, causing a huge number of potential buyers to get priced out of the market or, at least, reassess purchasing a home. As inflation continues to decline, the Fed has offered a clearer picture of their path. They will raise the federal funds rate through 2023 to around 5.5% and then lower rates by about 2% over the course of 2024 and 2025. Buyers, who are expecting to refinance, therefore, have more of a timeline for when they can expect lower rates. The monthly mortgage cost is reduced by 10% for every 1% decrease in the mortgage rate, so buyers can greatly reduce their monthly cost as rates fall.

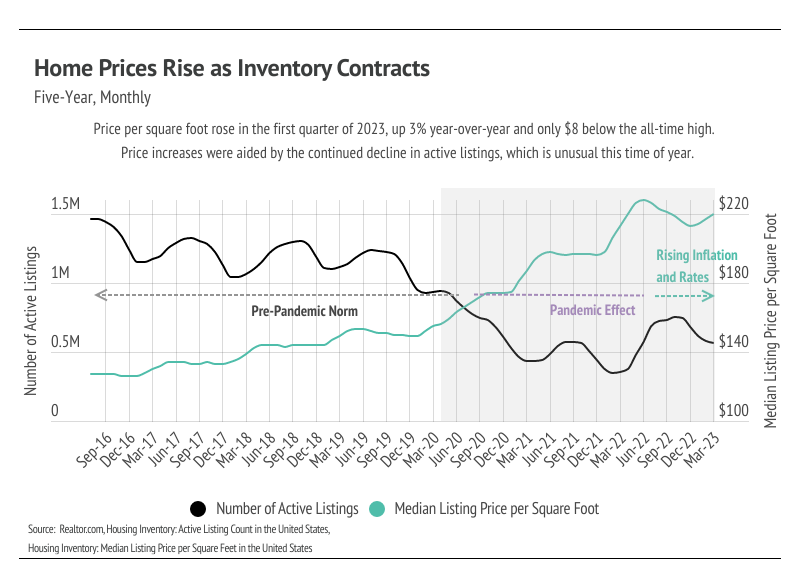

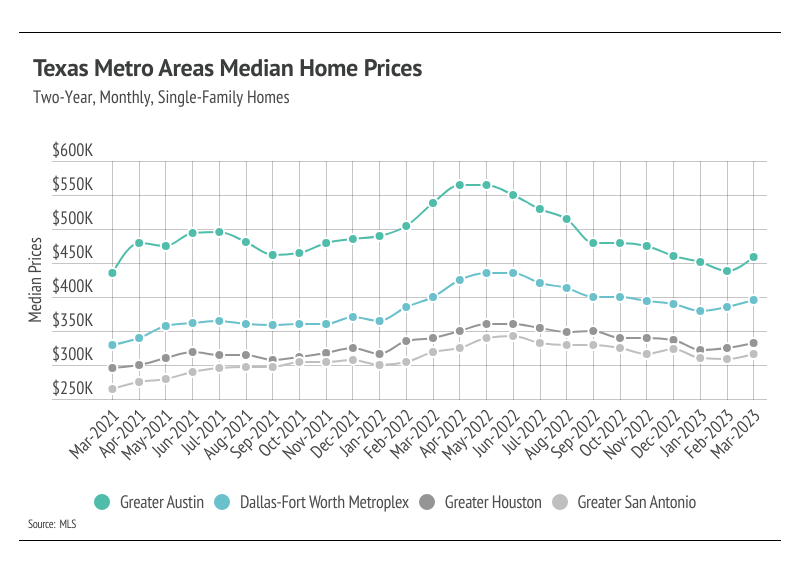

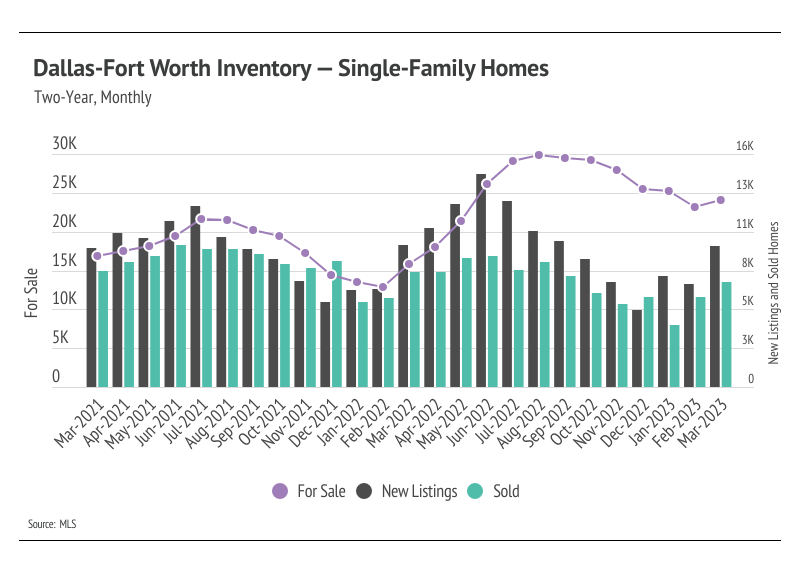

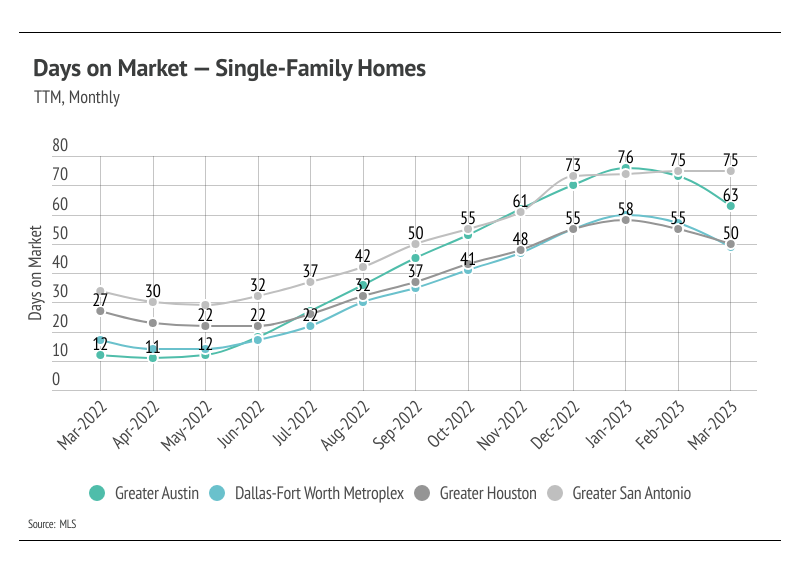

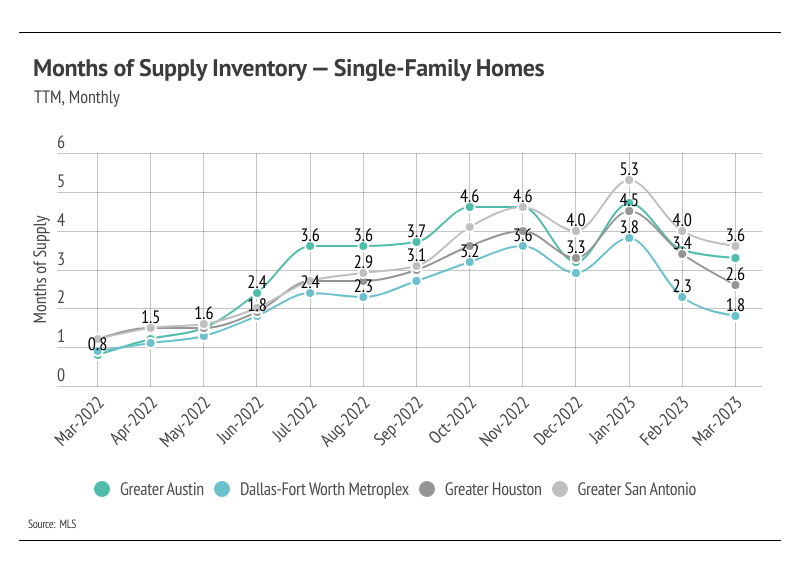

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage of your area. In general, higher-priced regions have been hit harder by mortgage rate hikes than less expensive markets due to the absolute dollar cost of the rate hikes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home. |

|

|

No comments :

Post a Comment